The truth is, budgets suck because they feel like punishment: a list of don’ts from Scrooge McDuck. But imagine, instead of this new budget that is more of a list of don’ts, there is one number that reflects you back that holds all sorts of insights into that number.

This is your Essential to Discretionary Expense Ratio. This is not about cutting pennies until they squeal. This is about achieving the kind of clear-sightedness that turns worries into options. I like to think of this in terms of the vision test for your finances. Then, suddenly, everything comes into focus.

Deciphering the Code: What We’re Talking About

Before we do the math, we’ll define our terms. This is the most crucial step, and honesty here requires a tender touch.

“Need-to-Pay” (Essential Expenses)

These are non-negotiables that help us keep the lights on, figuratively and literally. Without them, things get really tough, really quickly.

- The Usual Suspects: Rental or mortgage payment, utilities (electric, water, gas), basic grocery items, minimum debt repayment, commuting costs (car payment, gas card, transit card), and essential insurance (health, car).

- The Gray Area (Where Honesty Lives): This is where the rubber meets the road. Does your premium membership at the gym, which you only go to twice a month, qualify as a “need”? Is your current cell phone plan a “need” at the cost of $120 per month, or can you live with a plan for $60? Be honest with yourself. For me, the internet connection on my home computer qualifies as a “need” because it’s enabled telecommuting. For you, it may be your child’s school supplies.

“Choose to Spend” (Discretionary)

There’s your “flavor of life.” This is the latte drunk in the coffee shop, the TV series, the weekend getaway, the new book, dinner out. This category of expenditures will always be necessary, but there’s more than enough room to make some adjustments here.

The Golden Rule: Never depends on a panel of judges’ opinions. What may be optional for your neighbor may be a necessity for happiness for you.

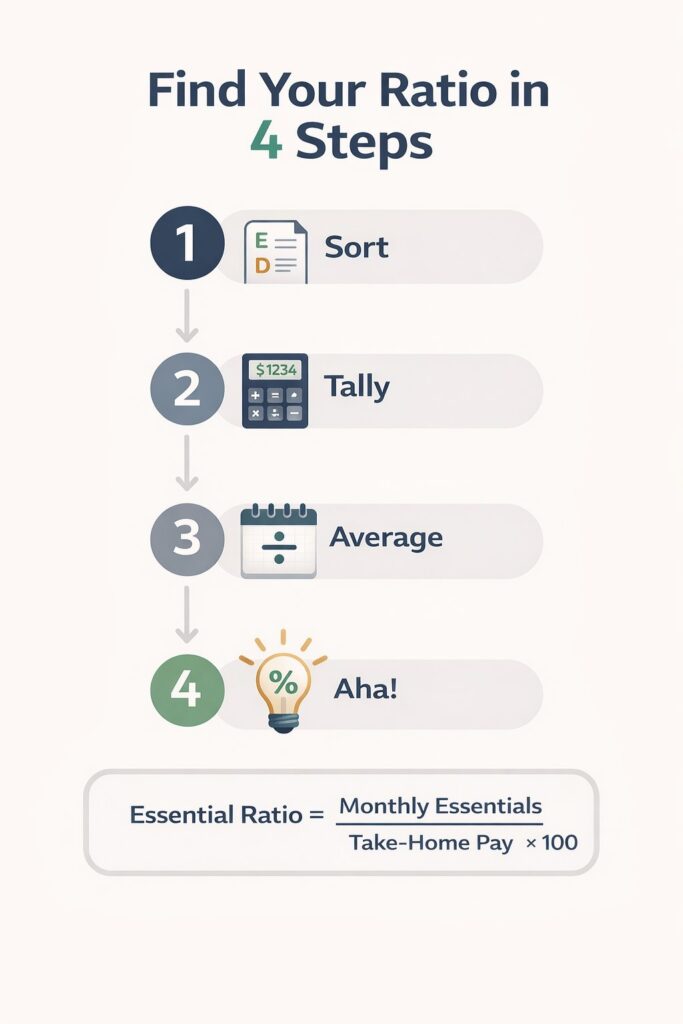

Find Your Number: A 20-Minute Kitchen Table Audit

Forget the complicated spreadsheets. What you will need is your last three months’ bank/credit card statements, to smooth out the irregular weeks, and a pen.

Step 1: Sort (No Overthinking)

Check each purchase. Just highlight it, make a little “E” or “D” in the corner with a highlighter. Groceries, E. Thu. night sushi, D. Electric bill, E. Video game purchase, D. Make the quick decision, and follow your intuition on the first choice.

Step 2: The Tally

Add together the three-month sum for each type.

- Total Essential Expenditures (3 months): $_____

- Total Discretionary Spending (3 months): $_____

Step 3: The Average

Calculate your average monthly expenditure.

- Average Monthly Essentials: (3-month total ÷ 3) = $_____

- Average Monthly Discretionary: (3-month total ÷ 3) = $_____

Step 4: “Aha!” Moment – Calculate Your Ratio

This is where the magic happens. Now, take your Average Monthly Essentials and divide it by your monthly take-home earnings.

Your Essential Ratio = (Monthly Essentials ÷ Monthly Take-Home Pay) x 100

My Example from Last Year:

My essentials were, on average, $2,900. My net salary was approximately $4,400.

(2,900 / 4,400) × 100 ≈ 66%

This meant that 66% of my income went into the necessary expenses. The remaining 34% is what I can decide to spend and save for later. It was such a relief to see that 34%, since I could actually decide where to allocate the amount.

So What? Interpreting Your Ratio Without the Panic

This number isn’t a grade. It’s a warning light.

- If Your Essential Ratio is High (Above 70%): You could feel some pain. You’re spending a lot on your essentials, leaving you with limited wiggle room. In this scenario, it could be more a question of either finding a way to make more money or perhaps figuring out a way to get a deal on that “essential” item or two.

- If Your Essential Ratio Is Lower (e.g., Below 50%): The reality here is you have a ton of wiggle room in your spending. It’s time for some strategy on how you’re spending that discretionary income. Is that 50 percent getting you closer to what you value most in life, or are you spending that 50 percent on fleeting moments of happiness?

The Real-World Superpower of Knowing Your Ratio

This is no abstract exercise. This figure becomes a useful instrument:

- It Helps Create a Realistic Safety Net: Remember that 3-6 month emergency fund? Now you understand that it should be sized not in relation to your income, but in relation to your actual expenses ($2,900 in my case).

- It Turns Guilt into Choice: The impact of seeing “34% discretionary” on paper was significant. I didn’t feel like I was “wasting” money on hobbies anymore; I was making a decision on how to allocate. I could also deliberately decide to allocate 5% back to my savings cushion.

- It Models Life Decisions: Think about relocating? Plug a new rent price into the equation. Thinking about becoming a freelance professional? With this formula, you can see just how much money you can actually make prior to considering desires.

The Bottom Line: Clarity Over Control

The calculation of this ratio has made me more comfortable with my finances than many budgets combined. It moved me from asking, “Can I afford this?” toward the more empowering question: “Is this expense aligned with my values?”

The point is not to get to some kind of optimal percentage. It is to go from financial fog to clarity. And it is from that clear space that something resilient can be built—on your own terms.

Disclaimer: This is from my own personal learning experience about money. This is awareness, not professional counsel. Your case may be different, and in big decisions, there’s always wisdom in speaking to a certified financial planner.