If you’ve ever wondered how much emergency fund do Americans need, you’re not alone. It’s one of the most common financial awareness questions in the United States. Many households notice that unexpected expenses rarely arrive at a “good time.” A car repair might cost $900. A medical bill might show up weeks after an appointment. A sudden job change can disrupt monthly income.

Understanding how much emergency fund do Americans need isn’t about chasing a perfect number. It’s about understanding what financial stability looks like in real American households and why having a buffer matters.

In this guide, we’ll break down the concept step by step, using realistic U.S. examples. This is about awareness, not advice — and about building clarity around one of the most talked-about financial topics in the country.

What Does “Emergency Fund” Really Mean?

Before answering how much emergency fund do Americans need, it helps to define the term clearly.

An emergency fund is money set aside specifically for unexpected, necessary expenses. It is not:

- A vacation fund

- A holiday shopping account

- A down payment fund

- An investment account

Instead, it is a financial cushion meant to protect households from disruptions.

In many U.S. households, common emergencies include:

- Car repairs ($500–$2,000)

- Medical deductibles or urgent care visits

- Home maintenance (HVAC repair, plumbing issues)

- Temporary job loss

- Sudden travel for family emergencies

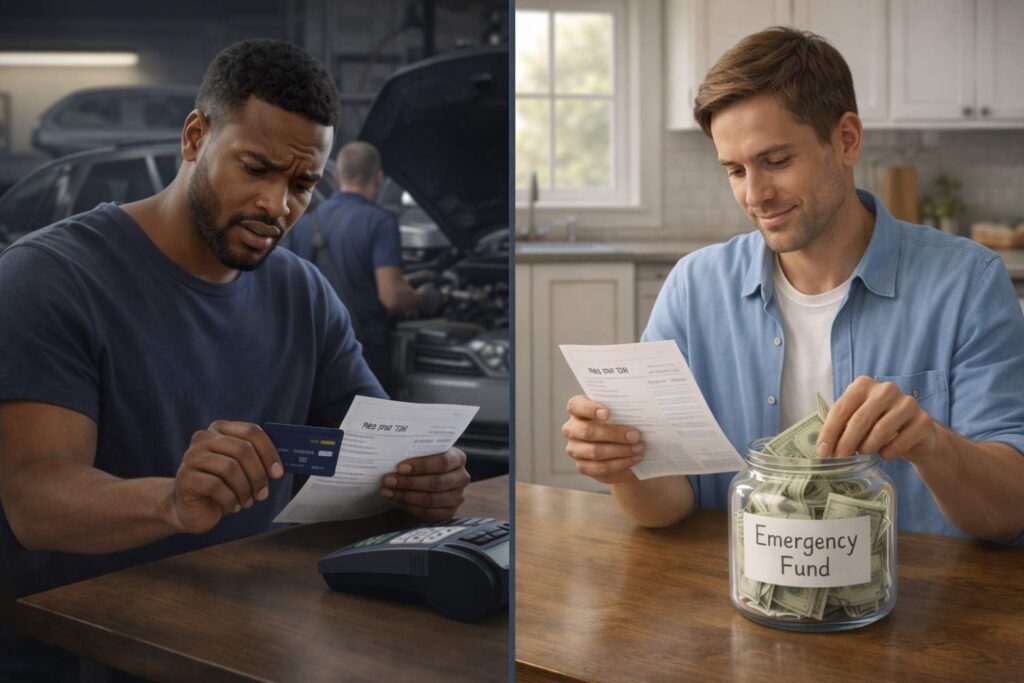

An emergency fund exists so that these situations do not automatically lead to high-interest debt.

How Much Emergency Fund Do Americans Need Based on Monthly Expenses?

When discussing how much emergency fund do Americans need, the conversation usually centers around monthly expenses.

A common situation in the U.S. is that fixed expenses make up the majority of a household’s budget. For example:

- Rent: $1,400

- Utilities: $200

- Groceries: $450

- Car payment: $350

- Insurance: $250

- Gas and transportation: $200

- Phone & internet: $150

Total monthly expenses: $3,000

If this household experiences a job interruption, they would need approximately $3,000 per month just to maintain basic living standards.

This is why emergency funds are often discussed in terms of “months of expenses” rather than a fixed dollar amount.

The 3–6 Month Awareness Benchmark

Many financial education discussions in the U.S. mention having three to six months of essential expenses saved.

Using the earlier example:

- 3 months = $9,000

- 6 months = $18,000

But it’s important to understand what this range represents.

Three months may provide short-term breathing room.

Six months may offer extended stability in uncertain job markets.

The idea behind this range is risk awareness:

- Dual-income households may face lower risk if one person remains employed.

- Single-income households may face higher risk during job disruptions.

- Freelancers and gig workers may experience more income variability.

So when asking how much emergency fund do Americans need, the answer often depends on income stability and monthly obligations.

Why Income Type Changes the Picture

Not all income is structured the same way in the U.S.

Salaried Employees

People with steady paychecks may experience predictable income. For them, a three-month cushion might feel stable, depending on job security.

Hourly Workers

Hours can fluctuate. Overtime may not always be available. A slightly larger buffer can reduce stress during slow periods.

Gig Workers & Freelancers

Income can vary month to month. Many independent workers notice that seasonal shifts or client changes impact cash flow. A longer emergency cushion often increases financial comfort in these situations.

Understanding your income pattern is part of understanding how much emergency fund do Americans need in your own household context.

Emergency Fund vs. Savings: Not the Same Thing

A common misconception in the U.S. is that “any savings” equals an emergency fund.

But general savings might be allocated for:

- Travel

- Holiday gifts

- Planned purchases

- Home upgrades

An emergency fund is specifically reserved for unplanned, necessary expenses.

Blending the two categories can create confusion. For example, if someone spends $2,000 from savings on a vacation, and then faces a $1,200 car repair, they may not have true emergency coverage.

This is why clarity matters when evaluating how much emergency fund do Americans need.

The Role of Cost of Living in Different States

Living costs vary widely across the United States.

In some cities:

- Rent may exceed $2,500 per month.

In other areas:

- Rent may be closer to $900 per month.

A household in New York City will naturally require a larger emergency cushion than a household in a smaller Midwest town.

Healthcare costs, insurance premiums, childcare, and transportation also vary by state.

That’s why asking how much emergency fund do Americans need without considering geographic cost differences can lead to unrealistic comparisons.

Healthcare Costs and Emergency Planning

Healthcare is one of the biggest unpredictable expenses for U.S. households.

Even with insurance, families may face:

- Deductibles

- Copays

- Out-of-network charges

- Prescription costs

A single emergency room visit can cost thousands of dollars before insurance adjustments.

Many households underestimate how quickly medical expenses can impact savings. Including potential healthcare costs in emergency awareness planning can provide a more realistic perspective.

Job Market Uncertainty and Financial Buffers

Job stability can change quickly.

Layoffs, company restructuring, or economic slowdowns can affect income unexpectedly. In recent years, many American workers experienced sudden employment changes.

When evaluating how much emergency fund do Americans need, job market volatility becomes part of the equation.

Some industries may have:

- Faster reemployment opportunities

- Stronger hiring demand

- Shorter unemployment periods

Other industries may require longer job searches.

Understanding your field’s hiring patterns adds context to emergency fund awareness.

What Happens Without an Emergency Fund?

When households lack a financial cushion, common responses include:

- Credit card reliance

- Personal loans

- Borrowing from friends or family

- Early retirement account withdrawals

Credit cards, for example, often carry interest rates above 20%. A $2,000 emergency expense can become significantly more expensive over time if carried as revolving debt.

Emergency funds reduce dependence on high-interest borrowing during stressful periods.

Smaller Emergency Funds Still Matter

Sometimes, conversations about how much emergency fund do Americans need can feel overwhelming. Hearing “six months of expenses” may seem impossible to reach for many families.

But smaller cushions still provide meaningful stability.

Even:

- $500

- $1,000

- One month of expenses

can reduce immediate financial shock.

Many households start with smaller milestones and gradually increase their buffer over time.

Financial awareness includes recognizing that progress is incremental.

Psychological Benefits of an Emergency Fund

Beyond numbers, there is a mental component.

Many Americans describe:

- Reduced anxiety

- Better sleep

- Increased confidence during job transitions

- Less stress when unexpected bills appear

Financial stability is not only about dollars. It’s also about emotional resilience.

When discussing how much emergency fund do Americans need, it’s helpful to recognize the psychological comfort that a financial cushion can provide.

Common Misconceptions About Emergency Funds

“I Have a Credit Card — That’s My Emergency Fund”

Credit cards provide borrowing power, not savings. Borrowed money must be repaid with interest.

“I’m Young, So I Don’t Need One”

Unexpected expenses do not depend on age. Car repairs, medical bills, and job disruptions can happen at any stage of adulthood.

“I’ll Start Later When I Make More Money”

Income increases do not automatically create savings. Many households notice that higher earnings often lead to higher expenses.

Understanding these misconceptions helps clarify why emergency savings discussions remain central in U.S. financial awareness conversations.

How Much Emergency Fund Do Americans Need in 2026 and Beyond?

Economic conditions shift over time. Inflation, healthcare costs, housing prices, and job markets evolve.

That means the question how much emergency fund do Americans need is not static. It should be revisited periodically as expenses change.

For example:

- If rent increases by $300 per month, emergency targets may adjust.

- If a household adds childcare expenses, monthly costs rise.

- If debts are paid off, required monthly coverage may decrease.

Emergency fund awareness grows alongside life changes.

A Realistic Example: Two Different Households

Household A

- Two working adults

- Combined income: $6,500/month

- Monthly expenses: $4,000

- Stable government jobs

They may feel comfortable with a three-month buffer of $12,000.

Household B

- Single parent

- Income: $3,200/month

- Monthly expenses: $3,000

- Retail job with variable hours

They may feel more secure aiming for a longer cushion, given income variability.

Both households are valid. The difference lies in risk exposure.

Building Awareness Without Comparison

It’s easy to compare savings numbers online. But social media often highlights extremes.

Financial awareness focuses on:

- Personal monthly costs

- Income stability

- Household size

- Local cost of living

Instead of chasing someone else’s number, clarity begins with understanding your own expense structure.

Final Thoughts on How Much Emergency Fund Do Americans Need

So, how much emergency fund do Americans need?

The answer depends on:

- Monthly essential expenses

- Income stability

- Industry job security

- Geographic cost of living

- Household structure

For many U.S. households, three to six months of essential expenses is a commonly discussed awareness range.

But even smaller buffers create meaningful financial breathing room.

Emergency funds are less about perfection and more about preparation. They exist to soften financial shocks, reduce debt reliance, and provide emotional stability during uncertainty.

Financial awareness begins with understanding where you stand today.

👉 use our Emergency Fund Builder to personalize your target

URL: https://smartmoneygate.com/emergency-fund-builder-gateway/

Frequently Asked Questions (FAQs)

1. Is three months of expenses enough for an emergency fund?

For some households with stable income and low debt, three months may provide short-term stability. Others with variable income may prefer a larger cushion. It depends on personal financial circumstances.

2. Should emergency funds include discretionary spending?

Emergency funds typically focus on essential expenses such as housing, food, utilities, insurance, and transportation, rather than entertainment or luxury spending.

3. Where do Americans usually keep emergency savings?

Many households keep emergency funds in accessible savings accounts to allow quick access while separating the money from daily spending.

4. Does inflation affect how much emergency fund do Americans need?

Yes. As rent, groceries, healthcare, and transportation costs increase, the amount required to cover several months of expenses may also rise.

5. Can retirement accounts serve as emergency funds?

Retirement accounts are generally intended for long-term savings. Early withdrawals may involve taxes or penalties and are not typically structured for short-term emergencies.

6. How often should emergency fund goals be reviewed?

It is common for households to reassess emergency savings when income, expenses, family size, or employment situations change.

Disclaimer:

This article is for financial awareness and educational purposes only. It does not provide financial, legal, or professional advice.