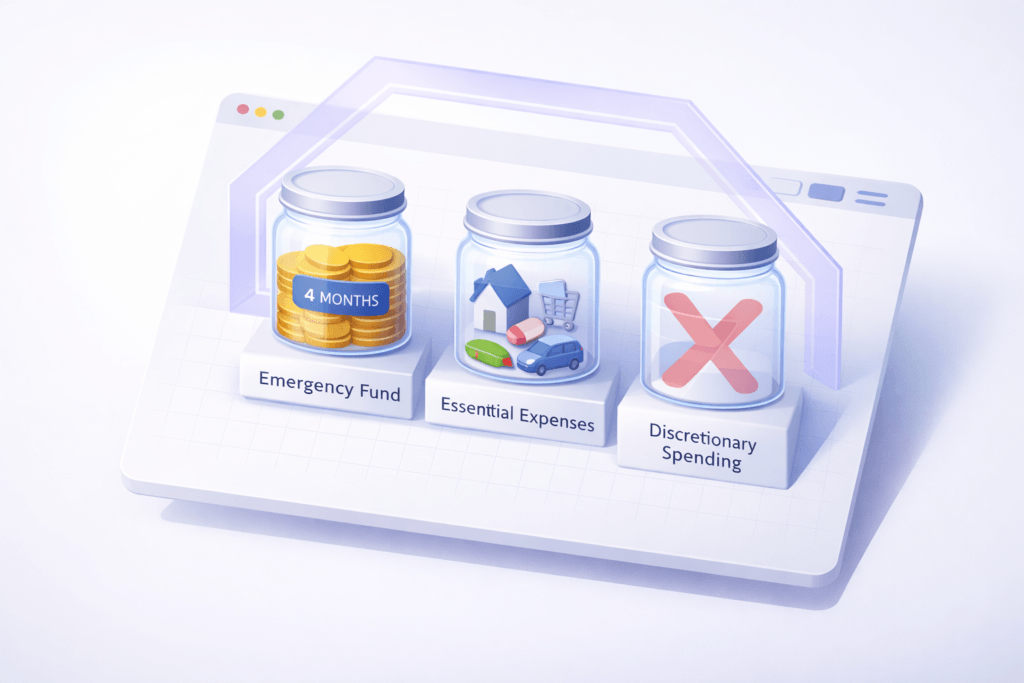

An emergency fund is “your financial airbag,” or Savings Buffer. You never, ever want to tap this money. However, when life throws a wrench (or car trouble, or healthcare issue, or even layoffs), this money is what keeps you from going bankrupt with high-interest debt. But just how much is “enough”? What Is an Appropriate Emergency Fund Size Based on Expenses?

It has nothing to do with what you are paid. It has everything to do with one thing: your true monthly expenses. This article will show you what size emergency fund you really need and exactly how to determine that without any advice or opinion, just facts.

Rule: *The 3-6 Month Rule*

The “3-6 Month Rule”

A typical rule of thumb is that one should save from 3 to 6 months of necessary expenses. But how is the term “necessary” defined here?

“Essential expenses are simply the costs you must pay in order to survive and remain protected,” he writes.

Rent or mortgage

Public Services (electricity, water, basic internet

Groceries

Minimum payments on debt

Transportation (car payment, gas, or bus fare)

Basic insurance (health, auto, renter’s

Do not include the following: streaming services, eating out, shopping, vacations, or hobbies. Your emergency fund is to survive—not to live.

For example, if your essential monthly expenditure is $2,500, your safety margin should be between $7,500 (for 3 months) and $15,000 (for 6 months

Who Needs 3 Months vs. 6+ Months?

This

It depends on your risk profile, not your income.

Target 3 months if you:

- Have steady, salaried employment

- Live in a dual-income household

- Provide health insurance and paid time off

Target for 6+ months when:

Freelance, gig, and commission work

- Are the sole earner in your household

- Manage chronic health problems

- Home ownership (with potential maintenance challenges)

- Live in a high-cost or economically volatile area

Freelancers and contractors may require a coverage period of 6-12 months because of irregular income sources and a lack of employer support.

Determine Your Essential Expenses

Essential expenses are those

Get the last 3 statements for your bank or credit card accounts. Add the minimum information. Calculate an average of the total amount. That’s your baseline.

Category of Expenditure

Rent

Utilities

Groceries

Car payment and Gas $300

Health Insurance

Minimum Debt Payment: $250

Total Essentials $

→ 3-month buffer = 7,500

→ 6-Month Buffer Price = **$

The Smart Money Gate Approach: Your Savings Buffer Gateway

At Smart Money Gate, instead of advice, we provide awareness. Walk through the Savings Buffer Gateway with questions like these:

“If my income were to suddenly disappear, how many months of my savings would pay my essential expenses?”

√a2 – b2

Savings Buffer (months) = Emergency Savings / Essential Monthly Expenses

Interpret your result:

< 1 month? → High risk. Begin with $500-$1,000 mini-buffer.

1 – 3 Months? → “Progressing well

3-6 months? → You have established baseline resilience.

6+ months? → You’re exceptionally well-prepared for income shocks.

Avoid These Common Pitfalls

============================

❌ Total income instead of essential expenses → Overestimation of your needs

❌ Keeping money in retirement savings instruments → consequences & market risks

❌ Using it for non-emergencies – This erodes the safety net.

❌ “Setting it and forgetting it” is a recipe for life change; your buffer zone must change with it

How to Build (or Rebuild) Your Buffer—Even on a Tight Budget

Start with the little things. For example, if you cut Automate Transfer of Funds into High-Yield Savings Account Make use of Windfalls such as Tax Refunds or Bonuses: Stop aggressive debt repayment if you have less than $1,000 saved Mark milestones: $1K => $3K => $6K => full buffer

Final Thought: It’s About Security, Not Perfection

What constitutes a “healthy” emergency fund? It isn’t a number, but a sense of well-being. Having even 1-2 months of coverage can turn a small glitch into nothing more than that. As the Be Debt-Free movement says: “Because financial peace isn’t about how much money you make, but how much money you keep.” It’s having the confidence to know you can handle what life throws your way—without swiping your credit card in desperation

And that? That’s priceless.

Disclosure: Please note that this piece is for educational purposes and should not serve as financial, investment, or professional advice. Smart Money Gate offers awareness services via Financial Awareness Gateways and not as investment ideas or any other form of investment decisions. It’s always important to seek advice from an appropriate expert for decisions concerning your personal finance.