I didn’t learn about Revenue Based Financing from a pitch deck or a finance blog.

I heard about it the way most useful things show up — casually. Someone mentioned it in a conversation that had nothing to do with funding. No hype. No “this will change your life” energy.

Just: “We didn’t want to give up equity, so we used revenue based financing instead.”

That sentence stuck with me longer than any investor meeting ever did.

Because if you’ve ever tried to fund a growing business, you already know the feeling: every option comes with strings. Heavy ones.

So let’s talk honestly about Revenue Based Financing — not as a trend, not as a magic solution, but as a practical tool that fits a certain kind of business at a certain stage.

First, what Revenue Based Financing really is (in real terms)

At its core, Revenue-Based Financing is simple.

A business gets capital upfront.

Instead of paying a fixed loan installment every month, it repays a percentage of its actual revenue.

That’s the defining feature.

When revenue is strong, repayments are higher.

When things slow down, payments shrink with them.

There’s usually:

- No equity given away

- No rigid repayment schedule

- A predefined repayment cap

Once you hit that cap, you’re done. Clean exit.

That structure alone puts Revenue Based Financing in a completely different category than traditional loans or venture capital.

Why this model exists in the first place

Here’s the thing most funding conversations ignore:

Businesses are uneven.

Some months are great. Others are weird. A few are just bad.

Traditional loans don’t care. Investors care, but often in ways that don’t help.

Revenue Based Financing exists because someone finally admitted that cash flow matters more than projections.

Instead of forcing businesses into fixed payments, RBF adapts to what’s actually happening.

That’s not revolutionary. It’s just… realistic.

Who Revenue-Based Financing tends to work for

Not everyone. And that’s important to say out loud.

Revenue Based Financing usually fits businesses that:

- Already make money

- Have reasonably predictable revenue

- Aren’t running on razor-thin margins

That’s why you see it used by:

- SaaS companies

- Subscription platforms

- E-commerce brands

- Agencies with recurring clients

- Creator-led businesses with steady sales

If your business is pre-revenue, this probably isn’t your option. And that’s fine.

But if you’re already operating and just need fuel to grow, Revenue Based Financing often feels less hostile than other funding routes.

Why founders quietly like Revenue Based Financing

Here’s something people don’t always say publicly:

A lot of founders don’t want investors.

Not because investors are bad — but because equity is permanent. Once it’s gone, it’s gone.

Revenue Based Financing doesn’t touch ownership. No dilution. No board seats. No explaining why you didn’t hit some arbitrary growth target in a slow quarter.

You run your business. The financing adapts.

That autonomy is a big reason Revenue-Based Financing keeps showing up in founder-to-founder conversations, even if it’s not always hyped online.

The uncomfortable truth: not all RBF deals are friendly

Now for the part that actually matters.

Revenue Based Financing as a model is solid.

Specific Revenue Based Financing deals? Not always.

Some providers:

- Take too high a percentage of revenue

- Set repayment caps that quietly hurt

- Make terms sound flexible but feel tight later

That’s why blindly choosing the first RBF offer is risky.

You don’t need faster funding.

You need clear funding.

Why tools matter more than offers

This is where something like the Sustainable Finance Gateways tool becomes useful.

Not because it promises money — but because it slows you down.

It helps you look at financing options through questions most people skip:

- What happens if revenue dips for three months?

- How does this affect long-term cash flow?

- Is growth still healthy under this structure?

Revenue Based Financing works best when it’s chosen intentionally, not reactively.

The tool helps keep the decision grounded.

A realistic starting point: Revenue Based Financing Gateway

If you’re exploring Revenue Based Financing and don’t want to dig through dozens of platforms blindly, this is a practical place to begin:

👉 Revenue Based Financing Gateway

https://smartmoneygate.com/revenue-based-financing-gateway/

It’s not positioned like a pitch. It’s more of a navigation point — a way to understand how Revenue Based Financing fits into the broader funding landscape.

And honestly, that’s what most founders actually need.

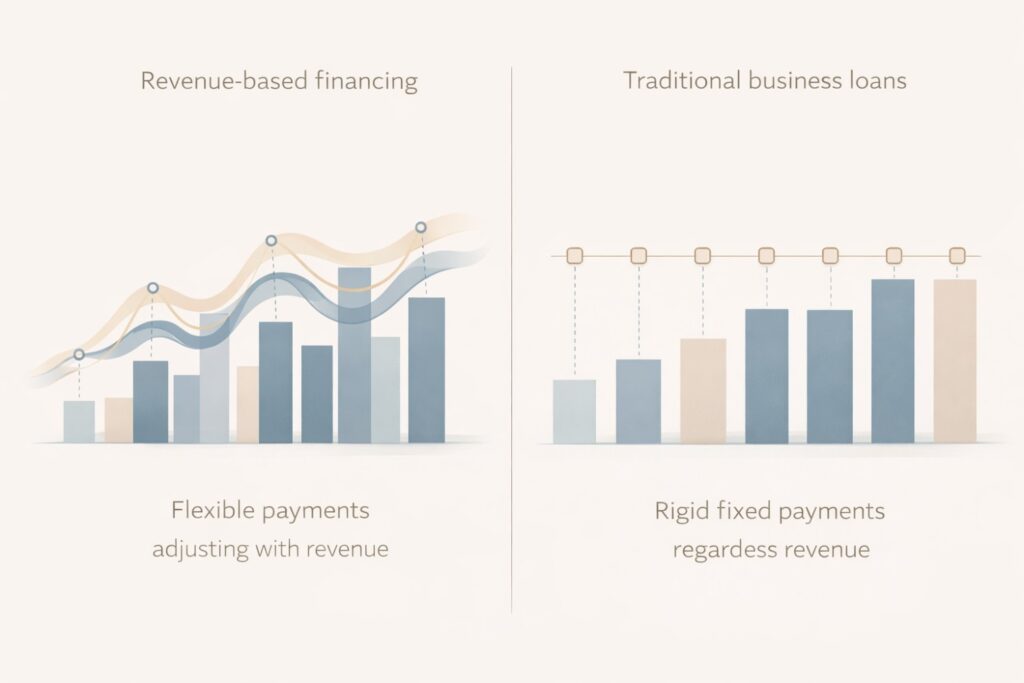

Revenue Based Financing vs traditional loans (from experience)

On paper, comparisons are easy. In reality, they’re emotional.

Traditional loans feel heavy.

- Fixed payments

- Stress during slow months

- Pressure to perform even when conditions change

Revenue Based Financing feels… lighter.

- Payments follow revenue

- Less panic when things dip

- More room to operate like a human business, not a spreadsheet

That difference shows up not just in numbers, but in decision-making.

Why Revenue Based Financing supports sustainable growth

This is the part I didn’t expect.

Revenue Based Financing quietly discourages reckless growth.

Because repayments scale naturally, you’re less tempted to:

- Overspend on acquisition

- Chase vanity metrics

- Push growth faster than systems can handle

When combined with thinking frameworks like the Sustainable Finance Gateways tool, it pushes businesses toward stability first, speed second.

That order matters more than people admit.

When Revenue Based Financing doesn’t make sense

It’s not a universal solution.

It might be the wrong choice if:

- Revenue swings wildly month to month

- Margins are extremely thin

- You need long, slow repayment timelines

In those cases, other funding options might be healthier.

The goal isn’t to force Revenue Based Financing.

The goal is to avoid funding that quietly hurts later.

Revisiting the Revenue Based Financing Gateway

If you’re even considering flexible funding — especially before you’re desperate — take a look here:

👉 Explore the Revenue Based Financing Gateway

https://smartmoneygate.com/revenue-based-financing-gateway/

Timing matters more than people think. Decisions made under pressure are rarely the best ones.

FAQs (No Corporate Voice, I Promise)

Is Revenue Based Financing just a loan with a new name?

No. The repayment structure changes the entire experience.

Do I give up equity?

No. Ownership stays with you.

What happens if revenue drops?

Payments drop too. That’s the design.

Is Revenue Based Financing expensive?

It can be if the terms are bad. That’s why comparison matters.

Can early-stage startups use it?

Only if they already generate revenue.

Final thoughts (nothing to sell here)

Revenue Based Financing isn’t exciting. It doesn’t make headlines.

But it respects reality. And that’s rare.

It respects:

- Uneven growth

- Cash-flow cycles

- Founder control

Used thoughtfully — with tools like the Sustainable Finance Gateways tool and a clear gateway into options — it can support growth without quietly draining a business.

That’s not flashy.

It’s just sensible.

Disclaimer

Disclaimer: This content is provided for educational purposes only and does not constitute financial, legal, or investment advice. Always consult a qualified professional before making financing decisions. Many founders exploring non-dilutive funding options also review guidance from institutions like the U.S. Small Business Administration before choosing a financing path.